Table Of Content

Some home buyers use down payment assistance (DPA) programs as part of their purchase. Down payment assistance programs cover most, or all, of the required mortgage down payment. According to estimates from Realtor.com, a home inspection costs anywhere from $300 – $500 for a single-family home.

Pay Off Debt

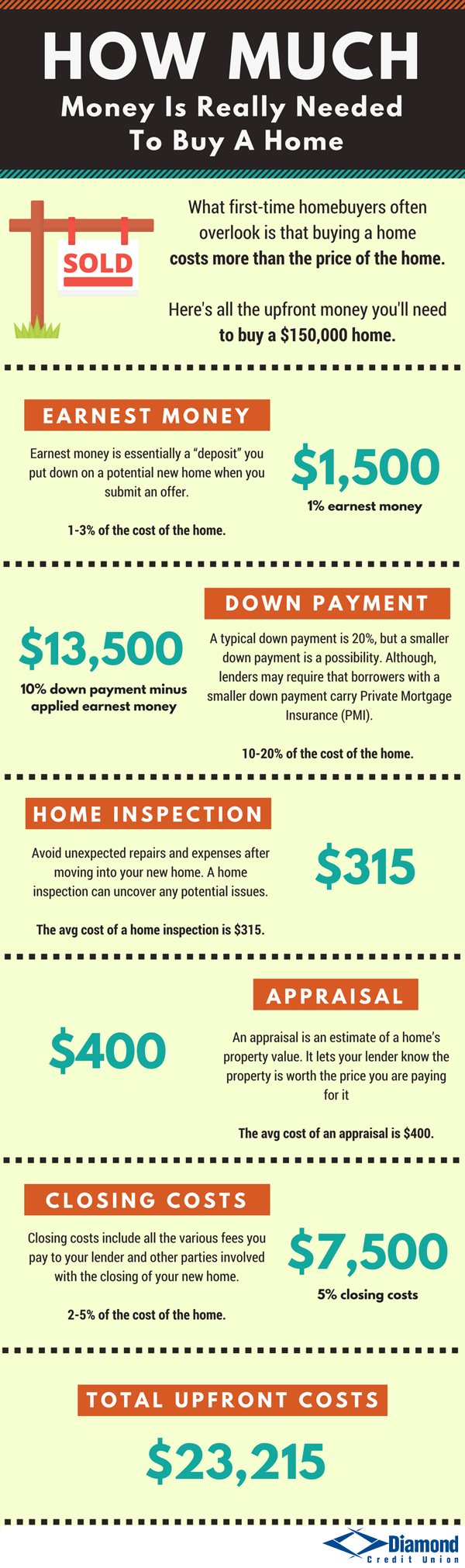

The upfront cash needed to buy a house includes the down payment, 2-5% of your loan amount for closing costs, and often at least two months worth of cash reserves. Here’s how much money you might need to save to buy a house, at a few different price points. And some mortgage lenders will give a credit to cover a borrower’s closing costs in exchange for a higher mortgage rate.

Moving Expenses

Homeowners with mortgages are required by the lender to secure the “asset” with homeowners insurance, and this cost will also be added to your monthly payment with the bank. Your existing debts will help determine how much money you can borrow to buy a house. High monthly debts (such as credit card debt, student loans, and other installment loans) could prevent mortgage approval.

Moving expenses: $1,000 or more

The average credit score needed to buy a house depends on the loan type. For conventional loans, it’s recommended to have a score of 620 or higher, while FHA and VA loans have a minimum credit score of 580. A good affordability rule of thumb is to have three months of payments, including your housing payment and other monthly debts, in reserve. This will allow you to cover your mortgage payment in case of an unexpected event.

For example, if you got that same $240,000 loan at a 7.0 percent rate, the payment for monthly principal and interest increases to $1,596. Key factors in calculating affordability are 1) your monthly income; 2) cash reserves to cover your down payment and closing costs; 3) your monthly expenses; 4) your credit profile. When figuring out how much you need to make to buy a $400K house, the 28/36 rule, a common real estate rule of thumb, is a good place to start.

Enough savings for the down payment and closing costs

Commonly cited best practice is to save up at least 20% of the purchase price, which is – at minimum – tens of thousands of dollars. It can be difficult to amass this amount in high-cost urban areas or for potential buyers with large student loan burdens. If you’re having trouble saving money, you might qualify for a down payment assistance program. These programs provide funds in the form of grants or loans, which you can use to pay your down payment and/or closing costs.

What is the average down payment for a house?

The best way to find out your total closing costs is to get a personalized estimate from a mortgage lender. A lender can provide a written estimate of your “cash to close,” which is the total amount of money you’d need up front to close your mortgage. The lender will also verify that you have, or will have, enough in your bank accounts to close the loan by looking at two months’ worth of your bank statements. In most cases, property taxes are pre-calculated by the mortgage lender and added to your monthly mortgage payment so the homeowner doesn’t get hit with an unexpected bill each year. When getting preapproved for a mortgage, you should contact at least three mortgage lenders to compare interest rates and terms.

We also want to know how you give them the money (cash, bank transfer, app) - and if they have to do anything in return. Gumtree's most popular items include rare stamps, Gameboys and Pokemon cards. Read this and all the latest consumer and personal finance news below, plus leave a comment or submit a consumer dispute or money problem in the box. Go.Compare has also broken its figures down to show the most and least affordable areas, depending on property type. Perhaps unsurprisingly, London comes out on top as the part of the UK that requires the highest salary across each category. If your move is local, this option will likely run you a few hundred dollars.

Maximum DTI varies by loan type

Other buyers will find conventional loans, with as little as 3% down, are better suited for their personal finances. That’s because higher-cost real estate often surpasses FHA and conventional loan limits. Borrowers must either make a larger down payment or opt for a jumbo mortgage to compensate.

Your DTI tells lenders whether you can afford to take on another debt. If your DTI is higher than 50%, you may have trouble getting a loan. If you’re on payroll, you’ll likely just need to provide recent pay stubs and W-2s. If you’re self-employed, you’ll need to submit your tax returns as well as any other documents the lender requests.

To buy a $250,000 house, you’d likely need to pay at least $16,750 upfront for a conventional loan. Upfront costs could be as low as $6,250 with a zero-down VA or USDA loan, though not all buyers qualify for these programs. Ask for a lender credit or alternative loan options to reduce your total out-of-pocket expense. You can also ask your Realtor or loan officer about non-profit down payment and closing cost assistance programs in your market.

Here's how much $ you need to make to afford a home in San Diego, per Zillow - NBC San Diego

Here's how much $ you need to make to afford a home in San Diego, per Zillow.

Posted: Thu, 14 Mar 2024 07:00:00 GMT [source]

And if possible, don’t switch jobs or make any big life changes, such as getting married, either. In general, for a 30-year fixed loan, you will have the lowest monthly payment but the highest interest rate. However, with a 15-year fixed, you’ll have a higher payment, but will pay less interest and build equity and pay off the loan faster. The average American home loan will cost anywhere from $2,162.46 to $3,482.12 per month, depending on the term of your mortgage and the down payment you make. Of course, that's assuming that your mortgage comes with today's average mortgage rate.

There’s no minimum income to get a mortgage, but some loan programs have a maximum income limit. Closing lines of credit can lower your score, so don’t completely shut down any credit you have. Also, avoid opening new credit while you’re trying to buy a home. Opening new credit can put a hard inquiry on your credit report, and too many hard inquiries affect your credit score. If your ratio is too high, start looking for places where you can cut back on your monthly budget or increase your income. The amount of money you earn is one of several factors considered in getting a mortgage.

Prospective buyers also pay an earnest money deposit to demonstrate serious intent to purchase a home. You’ll typically need to pay 1 percent of the home’s agreed-upon purchase price. But earnest money is not an additional expense, it’s just paying a bit of your expenses early. You make the deposit within a day or two after your offer is accepted, and at closing, it is credited toward your payment.

You'll need more than $100000 in income to afford a typical home, studies show - NPR

You'll need more than $100000 in income to afford a typical home, studies show.

Posted: Tue, 02 Apr 2024 07:00:00 GMT [source]

Start by checking your current home buying eligibility and comparing rate quotes from multiple lenders. When you’re serious about buying your dream home, the first step is to ask a lender for mortgage preapproval. Some of these requirements will vary based on the type of mortgage you choose.

This guideline advises that no more than 28 percent of your total income should be spent on your monthly housing costs, and that no more than 36 percent should be spent on monthly debt payments. Bankrate’s home-affordability calculator can help you figure out what salary is needed to afford a $400,000 home. Based on these numbers, your monthly mortgage payment would be around $2,470.