Table Of Content

You should consider paying down any existing debts such as student loans and credit card balances to lower your debt-to-income ratio prior to getting preapproved for a home loan. Buyers need to consider upfront costs like the down payment and closing fees, but also ongoing costs such as the mortgage payment, utility bills, homeowners insurance, and property taxes. To buy a house, you’ll need a qualifying credit score and debt-to-income ratio, proof of income and employment, and enough cash to cover the down payment and closing costs. Specific qualifying requirements will vary depending on your loan program and mortgage lender. Federal Housing Agency mortgages are available to homebuyers with credit scores of 500 or more and can help you get into a home with less money down. If your credit score is below 580, you'll need to put down 10 percent of the purchase price.

Mortgages

How Much Money Do You Need to Buy a House in 2024? - Credit.com

How Much Money Do You Need to Buy a House in 2024?.

Posted: Mon, 25 Mar 2024 07:00:00 GMT [source]

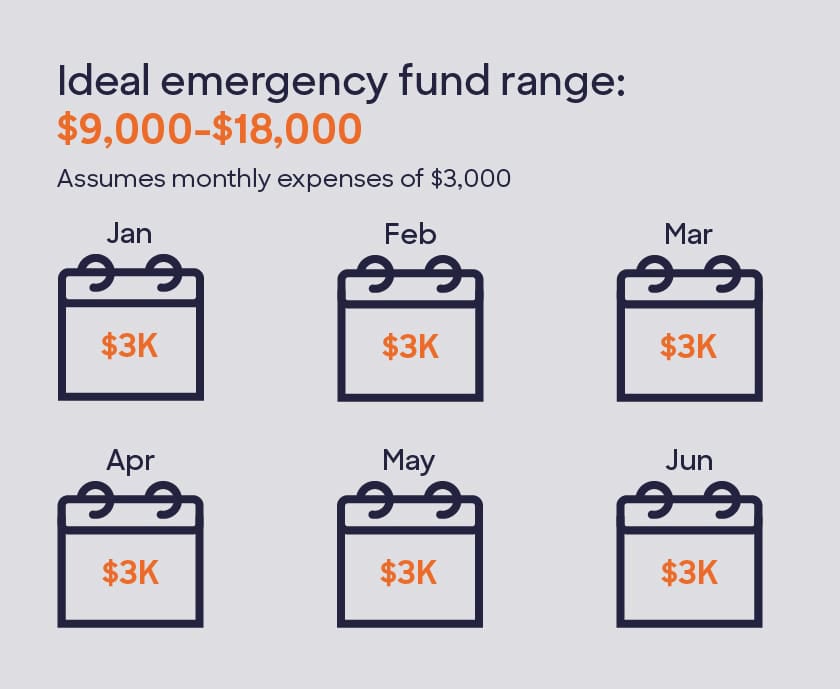

Even when looking at the numbers, Burbank Realtor Karol Kochova said buyers should resist the urge to panic. Across the United States, the average income needed to afford a home came in at $54,800. Over the length of the loan, though, the 15-year loan is a far better deal, considering the interest you pay — $514,715 in total. Each month we’ll pay $2,859.53, over 60% more than with the 30-year loan. When all’s said and done, for a 30-year loan at 3.5% interest, we’ll pay $1,796.18 each month. Finally, many experts suggest that you should have a meaningful emergency fund before you purchase a new home.

Property Taxes

When you’re planning your first-time home buyer budget, two percent would be a good estimate to use. To buy a house, you typically need 3 percent of the home price for a down payment and 1.5 percent for closing costs. So based on the typical U.S. home which sold for $356,700 recently, you could move into your first home with just $16,000 cash.

Cash reserves (0-6 months’ worth of mortgage payments)

This applies to self-employed mortgage borrowers, too, in which case you’ll provide your business and personal tax returns for the previous two years. Tax returns must show consistent income over the previous 24 months, either remaining roughly the same or increasing. “If you’re interested in bumping up your credit score, your lender may have the ability to help,” recommends Jon Meyer, The Mortgage Reports loan expert and licensed MLO. Even though a lender takes a look at your income stream when you buy a home, there’s no set income requirement to buy a home. A mortgage preapproval is a good first step to learn how much you can afford to spend on a home. A preapproval is also a smart move because you’ll be able to prove to sellers that you can get a loan.

Monthly Income

Before you know it, you’ll have a decent amount saved and ready for a down payment. As you’re thinking about how much money you need to buy a house, it’s crucial to know how much it will cost you every month, not just on closing day. An enduring nationwide housing shortage and the highest mortgage rates in more than 20 years might make you feel pessimistic about your chances of becoming a homeowner. Loans backed by the FHA can also have more relaxed qualifying standards — something to consider if you have a lower credit score. If you want to explore an FHA loan further, use our FHA mortgage calculator for more details. We believe everyone should be able to make financial decisions with confidence.

How To Budget For A House: A Guide For First-Time Buyers

Want to buy a house in Texas’ metro areas? Here’s how much you need to earn to afford one - KXAN.com

Want to buy a house in Texas’ metro areas? Here’s how much you need to earn to afford one.

Posted: Sun, 22 Oct 2023 07:00:00 GMT [source]

If you’re ready to begin your homeownership journey, getting preapproved is one of the first steps. Mortgage preapproval helps you identify your budget and find out what you qualify for. Depending on the loan program, you may be able to buy a house with less money out of pocket than you think. New homeowners often underestimate the amount of cash they’ll need both upfront and after the home sale closes.

Rocket Sister Companies

Because the closing costs are rolled into the amount of the mortgage, you're borrowing more money — and paying interest on all of it. The seller typically pays for a few, such as the commission for the real estate agent and often, a real estate transfer tax. However, it’s important to consider closing costs and other home-buying fees that you’ll need to pay for as well. That’s why you should speak with a professional mortgage expert or your real estate agent to make sure you’re making a down payment you can afford. There’s no one-size-fits-all answer for how much you should spend on your first home.

How much house can I afford with an FHA loan?

However, shopping for your new home and getting an offer accepted can take months. The amount of time it takes you to buy a house will depend on how long you look for a home, plus time spent closing on the mortgage loan. Be mindful, too, of possible income requirements for the type of loan you want. There’s typically no minimum income requirement, but you can earn too much money for some first-time home buyer programs.

Not to mention, until you own your home, your monthly payments do nothing in terms of building equity. Home prices have been on a rollercoaster ride in recent years and are still very high, as are mortgage rates. It’s enough to make you wonder whether now is even a good time to buy a house. It’s important to focus on your personal situation rather than thinking about the overall real estate market. Is your credit score in great shape, and is your overall debt load manageable?

Paying a lower interest rate in those initial years could save hundreds of dollars each month that could fund other investments. Your interest rate and monthly payment will increase after the introductory period, which can be three, five, seven or even 10 years, and can climb substantially depending on the terms of your loan. The National Association of Realtors suggests that the average down payment on a home for first-time buyers is about 6%, while repeat home buyers put an average of 17% down. That works out to about $25,860 for first-time buyers and $86,200 for repeat buyers based on the average price of a home in today's market. According to data from the United States Federal Reserve, the average home in the United States costs $431,000.

That’s because mortgage lenders typically collect four to six months of property taxes upfront. Taxes vary widely based on the home’s market value, and there is a big cost difference between a house with $100 in monthly taxes and a house with a $500 monthly tax bill. The upfront costs of buying a home will vary a lot depending on things like the home value, the type of mortgage, and where you buy real estate.

Some loan types, such as FHA loans, accept lower scores, but a higher score will almost always get you the lowest available interest rate. And that could save you a significant amount over your loan term. If your credit score has room for improvement, take this time to work on it by making on-time debt payments and paying off extra debt, if you have the room in your budget. And be sure to stay on top of your credit score throughout the mortgage process. There are many costs involved in the process of buying a home, from the down payment and closing costs to homeowners insurance and repairs.

A preapproval will give you a reasonable budget to use when you start shopping for a home. Once you know your target budget, you can browse homes for sale to see what general prices are. It’s a good sign you’re ready to buy if you find appealing options at your price range.

For more on the types of mortgage loans, see How to Choose the Best Mortgage. It follows interest rates stabilising, Halifax says, after a sharp rise over the past two years which squeezed mortgage affordability. A demand for smaller homes has driven growth in UK property prices early in 2024, according to research by Halifax. The Zoopla research looked at the average home buyer taking out a 70% loan-to-value mortgage. The full range will be available in Waitrose shops, Waitrose.com and Ottolenghi.co.uk from today, while a selection of products will be available from the supermarket on Deliveroo and Uber Eats.

No comments:

Post a Comment